The Enterprise Investment Scheme (EIS) is now over 20 years old. Reaching this milestone is quite remarkable for a tax break as a change in government often results in the demise of one tax break to pave the way for a ‘new and better’ one. Here we look at why EIS is worth the consideration of companies and investors.

Who is EIS for?

Despite a few amendments over the years, the aim of EIS has always been to help smaller trading companies raise finance by offering a range of tax reliefs to investors who purchase new, full-risk ordinary shares.

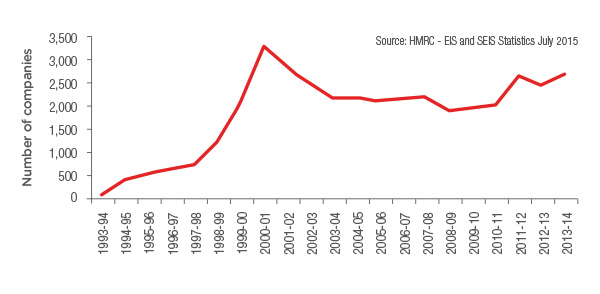

The chart above shows the number of companies raising funds in the first 20 years of the scheme, with the peak in 2000 reflecting the dot-com boom. In 2013/14, 2,710 companies raised a total of £1,457 million of funds under EIS.

Two of the key tax breaks are:

• income tax relief – investors may be given income tax relief at 30% on their investments of up to £1,000,000 a year

• CGT exemption – gains on the disposal of EIS shares are exempt from Capital Gains Tax.

For many investors who are new to a company, these reliefs may be the key additional incentives to invest. The income tax relief enhances the effective dividend yield that is anticipated from the investment. The CGT exemption removes gains from a charge to tax, without limit, on shares that have qualified for income tax relief. Therefore, companies wanting to raise finance for a new venture should consider whether the EIS scheme could apply to them. New companies can also consider the junior sister of EIS, the Seed Enterprise Investment Scheme (SEIS).

Neither tax break will be available if the person is ‘connected’ to the company, for example if the potential investor already controls more than 30% of the ordinary share capital of the company. If a number of individuals are setting up a new venture, an EIS or SEIS scheme could provide tax breaks for any of the individuals who hold less than 30% of the shares.

Where funds needed to establish the new venture are relatively small, the business owners may consider that the time and cost involved in setting up an EIS or SEIS scheme is not worthwhile when offset against the potential gains. But they should not forget the power of the CGT exemption as demonstrated by the recent tax case of the unfortunate Mr Ames.

The skydiver

Mr Ames was a skydiver. Realising that the risks and costs of the sport, together with the British weather, limited the growth of his sport in the UK, he had the idea of teaming up with a small number of other individuals to provide the first UK indoor skydiving simulator.

The company applied for share subscriptions to fall within EIS. HMRC agreed and the company issued Mr Ames with the relevant form for him to submit to HMRC. He never completed the form because, although he had paid £50,000 for his shares in 2005, his income was below the personal allowance for that year and the preceding year.

The company prospered and Mr Ames was able to sell his shares for £333,200 in 2011. When he submitted his tax return for the disposal he submitted the EIS form.

HMRC accepted that all relevant EIS conditions had been met and said that, had Mr Ames made a claim for EIS income tax relief, no CGT would have been payable on the disposal of the shares. However, Mr Ames had not made a claim and was no longer within the time limit. So the capital gain of £283,200 was taxable rather than tax free. The tax tribunal agreed with HMRC.

If you would like to know more about EIS or other business investments and reliefs, please contact your RfM advisor.