An increase in the personal allowance, set out in the UK Budget, came into effect on 6 April 2018. Changes to the basic rate threshold mean taxpayers in England can also earn more before the higher rate of tax kicks in. The story is slightly different for Scotland and Wales. Here we give you the headline figures.

The personal allowance for taxpayers in England has been increased from £11,500 in 2017/18 to £11,850 in 2018/19. So you can earn an extra £350 a year before you have to pay any tax at all.

The basic rate band has risen from £33,500 in 2017/18 to £34,500 in 2018/19, meaning that the threshold for the higher 40% band has increased from £45,000 to £46,350, for those entitled to the full personal allowance.

Tax rates for Scottish and Welsh taxpayers

For taxpayers treated as resident in Scotland, it’s a different story. In 2017/18, the basic rate income tax band for Scottish residents is £31,500. This excludes savings and dividend income for which the £33,500 basic rate band applies. This difference means that Scottish taxpayers will generally pay higher rate tax if their income exceeds £43,000, or if total income (including savings and dividend income) exceeds £45,000.

The Scottish Budget 2018/19 proposals include new tax rates and also new bands – making a total of five tax bands in all. The rates and tax bands for 2018/19 for Scottish taxpayers on income (except savings and dividend income) are expected to be as follows:

The above figures assume the individual is entitled to the full UK personal allowance. If an individual’s adjusted net income is above £100,000, the personal allowance will be reduced. In this case it is reduced by £1 for every £2 earned over £100,000.

There is a special S tax code for Scottish taxpayers. This should be issued by HMRC and employers should not make decisions on residence status. If you have questions on this area, or any other aspect of employer payroll procedure, please contact us for advice.

There are also changes to tax rates on the horizon for Welsh taxpayers. New Welsh rates of income tax are expected to be introduced from 6 April 2019.

Keep HMRC informed

We recommend that employers prompt their employees – Scottish or Welsh – to make sure HMRC have their up-to-date address details. An individual can notify HMRC of any changes, and check details currently held, online via the Personal Tax Account. Direct your employees to the gov.uk website to set up a Personal Tax Account or sign in to an existing account.

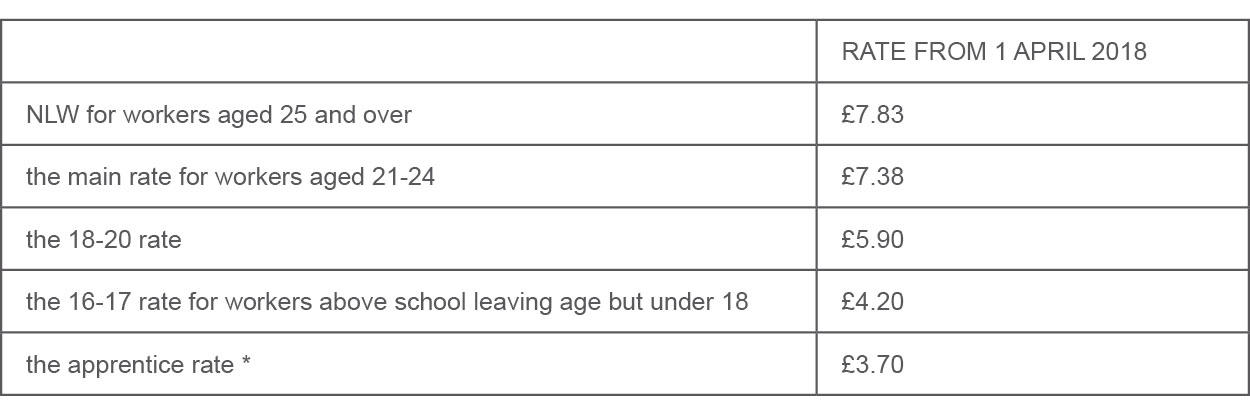

New National Minimum Wage (NMW) rates from 1 April 2018

New NMW rates came into effect from 1 April 2018; the biggest rise for workers under 25 for a decade.

The rate of pay for 18-20 and 21-24 year-olds has risen by 4.7% and 5.4% respectively. Those aged 25 and over should also benefit from a 4.4% increase in the National Living Wage (NLW).

NMW and NLW vary depending on age and whether or not a worker is an apprentice.

*for apprentices under 19, or 19 or over and in the first year of their apprenticeship

Please note, there are no exemptions from paying NMW on the grounds business size. Failure to pay NMW could result in financial penalties, potential prosecution and the risk of being named and shamed.

For information of users: This material is published for the information of clients. It provides only an overview of the regulations in force at the date of publication, and no action should be taken without consulting the detailed legislation or seeking professional advice. Therefore no responsibility for loss occasioned by any person acting or refraining from action as a result of the material can be accepted by the authors or the firm.